💵 Southeast Asian currencies show diverse performance amid uncertainty

Global conflicts, trade wars and domestic sentiment trigger swings that weaken or strengthen local currencies

🎯 The Main Takeaway

Southeast Asian currencies showed varied performance in 2025 and in the first month of 2026. Some gained appreciation, while others experienced depreciation, depending on global and domestic conditions.

📡 Why It’s On Our Radar

Several major global events occurred last year, with some still ongoing today:

💰 Federal Reserve rate cuts: The Federal Reserve decided to cut its interest rate three times—in September, October, and December 2025—by 25 basis points each, bringing the policy rate down from 4.25–4.50% to 3.50–3.75%.

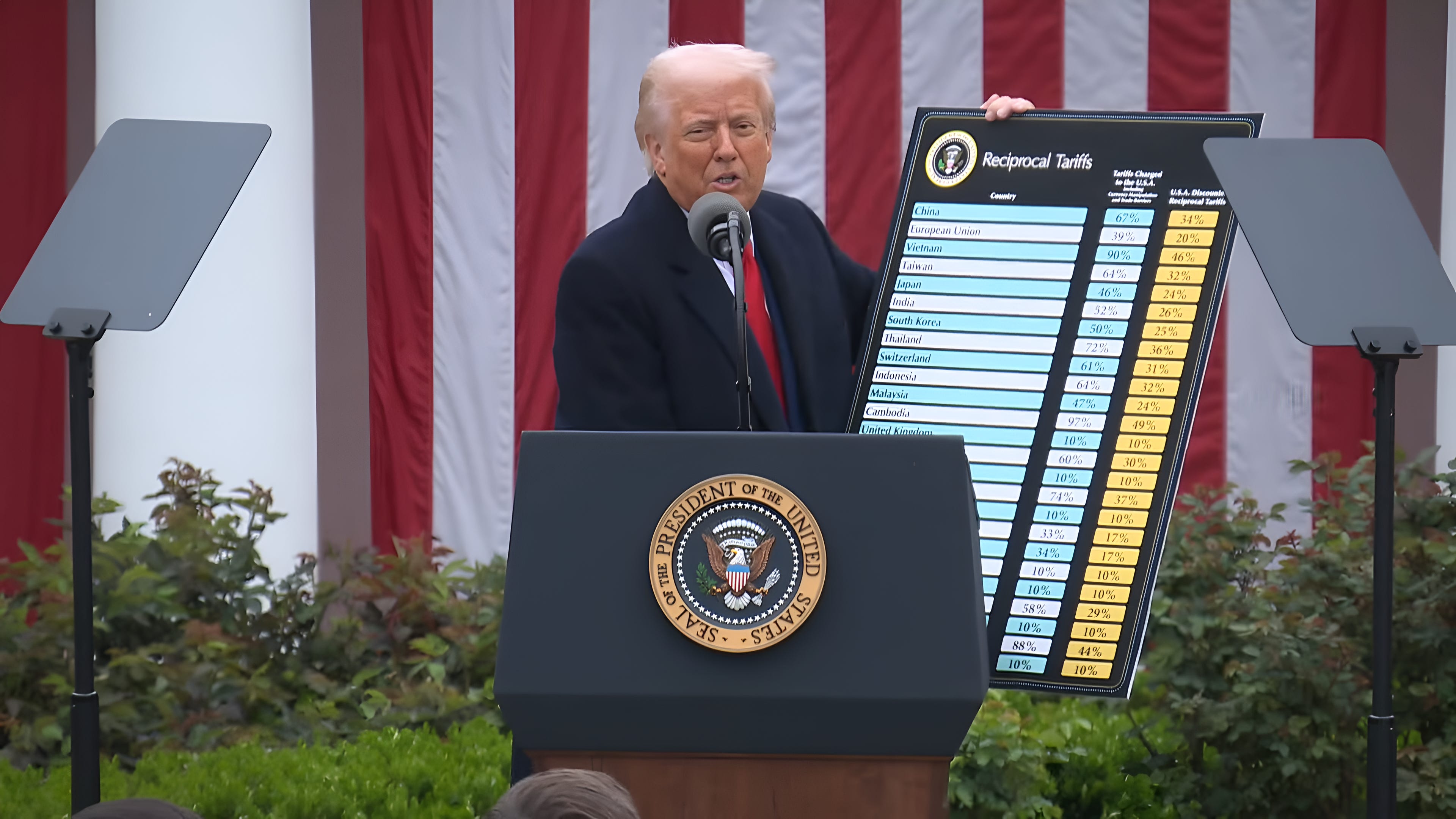

📋 Trump tariff policy: U.S. President Donald Trump announced a reciprocal tariff policy on April 2 last year, imposing additional tariffs of 10–50% on imports from all U.S. trading partners, depending on the U.S. trade deficit with each country.

⚔️ Geopolitical risks: Ongoing conflicts from the Middle East to Myanmar have driven demand for gold as a safe haven, often at the expense of local tenders.

💸 Central Bank Independence: Market sensitivity to political interference has triggered rapid capital outflows.

⚠️ Why It Matters

These global events potentially affect local currencies in Southeast Asia due to:

📉 Weaker U.S. dollar: Lower interest rates mean lower returns on U.S. Treasury bonds, prompting capital outflows to other emerging markets; this strengthens local currencies while weakening the U.S. dollar.

📈 Capital inflows: Capital inflows into emerging markets in Southeast Asia—including investments in bonds and stocks—may strengthen local currencies.

💸 Commodity price hikes: Ongoing global conflicts have driven up commodity prices and fuelled inflation, potentially weakening local currencies.

🚢 Export shifts: President Trump’s reciprocal tariff policy may reduce exports to the U.S., leading to lower export revenue and weakening local currencies.

💼 Asset shifts: Ongoing global conflicts, uncertainty, and economic instability have increased demand for gold as a safe-haven asset, which may weaken local currencies.

🔑 Key Highlights

🇧🇳 Brunei Darussalam: Strengthen ~5% in 2025 (USD 1 = BND 1.26), remained stable on Jan 26 (USD 1 = BND 1.26), driven by stable domestic condition (GDP grew by 0.03% in Q3, low inflation (below 1%), and political stability.

🇰🇭 Cambodia: Fluctuative but stable in 2025 (USD 1 = ~KHR 3,900), then weakened by 0.7% as of Jan 26 (USD 1 = KHR 4,000), driven by an active monetary policy using foreign exchange market intervention through buying and selling U.S. dollars, along with the widespread use of the U.S. dollar for most transactions.

🇮🇩 Indonesia: The rupiah weakened to IDR 16,700 despite a trade surplus; net outflows reached IDR 5.96 trillion this month following concerns over Bank Indonesia's independence.

🇱🇦 Laos: Relatively stable, strengthen ~1% in 2025 (1 USD = LAK 21,400), then weakened 0.27% in Jan 26 (1 USD = LAK 21,500), driven by strict monetary policy by increase interest rates, manage debt, increasing reserve and control foreign exchange transaction to maintain pressure on LAK.

🇲🇾 Malaysia: The strongest in Asia; strengthened ~10% in 2025 (USD 1 = MYR 3.9), backed by 5.2% GDP growth and a massive trade surplus.

🇲🇲 Myanmar: Stable, driven by the military junta’s policy of setting the official exchange rate at MMK 2,100 per USD from 2022; however, the exchange rate may reach around MMK 4,000 per USD on the black market.

🇵🇭 Philippines: Depreciated to PHP 59.15 due to a large trade deficit and political uncertainty surrounding the Vice President’s impeachment attempt.

🇸🇬 Singapore: Up ~1.4% this month (USD 1 = SGD 1.26), benefiting from its status as a stable financial hub and an alternative safe haven.

🇹🇭 Thailand: Resilient tourism and a USD 20.4 billion trade surplus pushed the baht to THB 31.05 per USD.

🇹🇱 Timor Leste: No local currency, with the U.S. dollar used as the official currency since 2000.

🇻🇳 Vietnam: Recovering slightly to VND 26,100 on the back of strong FDI inflows totaling USD 28.54 billion.

📊 What at Stake

Local currency performance in ASEAN has several major effects on economic and financial activity in the region:

📈 Inflationary pressure: Weaker currencies are eroding local purchasing power as import costs rise.

🤝 Investor confidence: High volatility is pushing portfolio investors toward more predictable markets.

💳 Debt burden: Depreciation is making U.S. dollar-denominated debt significantly more expensive to repay, straining state budgets.

🔀 Policy trade-offs: Central banks may be forced to raise interest rates to defend local currencies, which can slow economic growth.

🏡 Why This Hits Home?

ASEAN is now the 5th largest economy globally, with a GDP of USD 3.9 trillion. Because the region is a global supply chain hub, currency stability directly dictates the cost of living and the success of local trade. In 2024, regional trade reached USD 3.8 trillion, making every basis point of currency movement critical for business margins.

💡 What does ASEAN need to do

Guard Independence: Ensure central banks can set policy without government intervention to anchor investor trust.

Diversify Products: Shift from raw materials to higher-value exports to boost revenue resilience.

Enhance Cooperation: Expand local currency settlement to reduce the hidden vulnerability of U.S. dollar dependence.

🧭 Beyond the Headline

Confidence beats numbers. Macro data like GDP growth is secondary if investors doubt a nation's policy credibility. Markets react faster to political risk and fiscal discipline than to headline economic figures.

In short, exchange rates reflect trust as much as they reflect economics.

🔮 The Bottom Line

Southeast Asian currency is not just about economic growth, but about confidence, policy consistency, and resilience to global volatility.

Strengthening fundamentals, safeguarding central bank independence, and deepening regional cooperation are key for ASEAN to reduce vulnerability and sustain currency stability in the future.

🔎 Need More Angles?

ASEAN Secretariat ASEAN Investment Report 2025

ASEAN Stats ASEAN Statistical Highlights 2025

ASEAN+3 Macroeconomic Research Office Lao PDR: Strengthening Economic Stability Through Policy Support and Reform

Bangko Sentral Ng Pilipinas BALANCE OF PAYMENTS REPORT 3rd Quarter 2025

Bank Indonesia Perkembangan Indikator Stabilitas Nilai Rupiah (2 Januari 2026)

Bloomberg Technoz BI: Modal Asing Rp125 T Keluar dari Indonesia Sepanjang 2025

Malaysian Ministry of Finance Economic Momentum Expected To Continue In 2025 Following Strong Expansion In The Third Quarter

MBSB Research Ringgit Ended the Year 2025 with A Strong Performance

Nation Thailand Foreign tourist arrivals to Thailand in first 9 months of 2025 drop 7.5%

The Federal Reserve Federal Reserve issues FOMC statement

Voice of Vietnam Nine-month FDI hits US$28.54 billion, up 15% year on year

(NGO/ELS)